0.05%

0.05%

In March Bloomberg Aggregate Bond Index

0.50%

In March Bloomberg U.S Corporate High Yield Index

Geopolitical and Economic Update:

War with Iran Takes Center Stage

The continued war in Iran was the primary news story throughout the month, and rapidly developing headlines grabbed investor attention and led to choppy returns. The month served as a good reminder that markets face a variety of risks that can unexpectedly develop at any time. While the initial reaction to the strikes at the end of February was muted, markets swung throughout March on war-related headlines and updates.

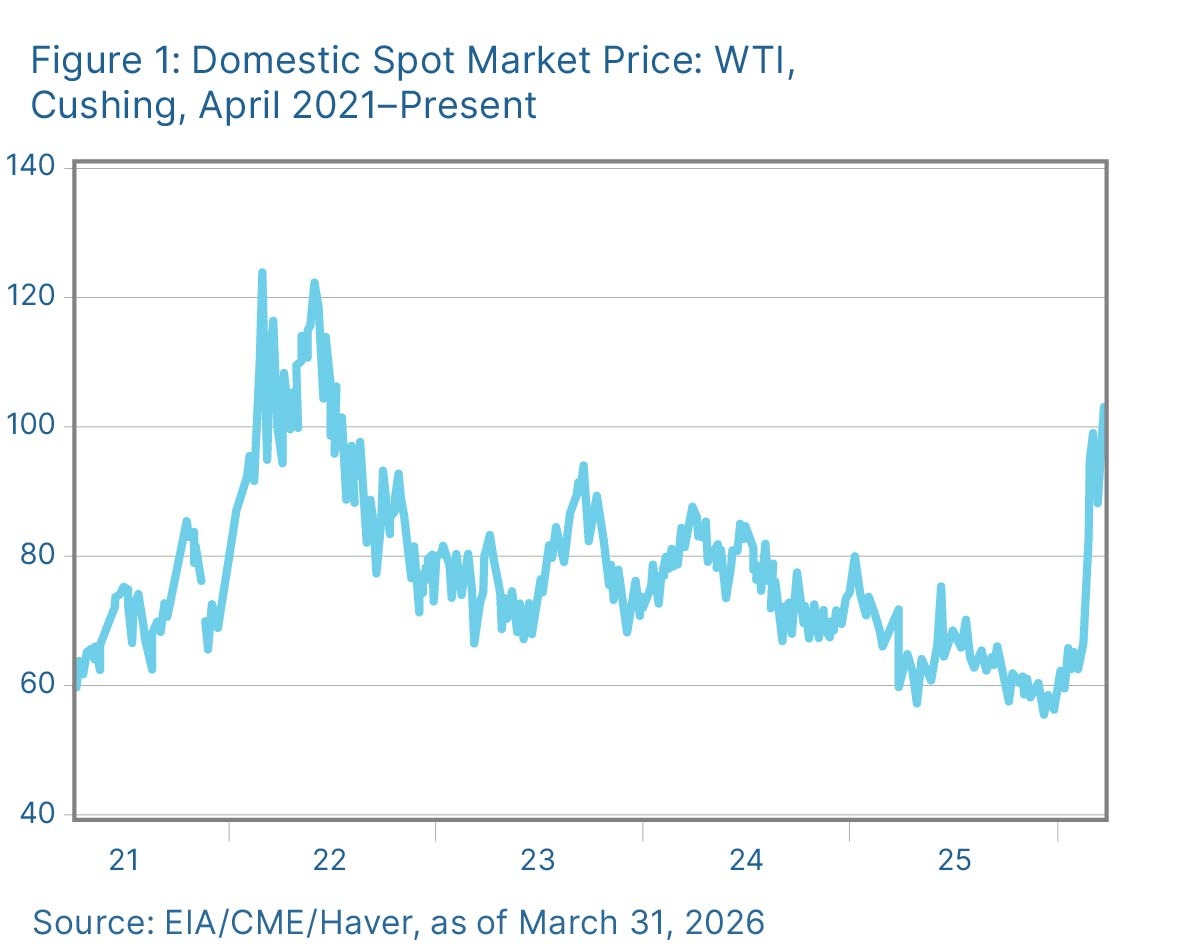

Energy prices remained high and volatile throughout March, with rising crude oil prices in the spotlight. As seen in Figure 1, domestic oil prices rose to over $100 a barrel toward the end of the month, which is the highest we’ve seen since 2022 following the Russian invasion of Ukraine. If higher energy prices persist, this would likely serve as a headwind for future economic growth and lead to rising inflationary pressure.

Rising energy prices have already started to have an impact on other areas of the economy. Consumer sentiment fell to a three-month low in March due in part to rising short-term inflation expectations. The survey showed that consumers expect prices to rise by 3.8 percent over the next year, up from 3.4 percent in February. Gas prices were up by roughly $1 on average during the month, and pain at the pump could start to negatively impact discretionary consumer spending in the months ahead.